Multi-Employer Benefit Plan Council of Canada

July 27, 2020

Michael Peters

Acting Superintendent of Pensions

BC Financial Services Authority

michael.peters@ficombc.ca

Multi-Employer Benefit Plan Council of Canada

Paul Owens

Deputy Superintendent of Pensions

Government of Alberta.

paul.owens@gov.ab.ca

Re: Alberta and British Columbia PfAD Analysis Applicable to Target Benefit Plans and Collectively Bargained Multi-Employer Plans

Alberta and BC each introduced Provision for Adverse Deviations (PfADs) in conjunction with the elimination of solvency funding which, we understand, was intended to be a bridge between unrestricted going concern funding rules and rigid, onerous, solvency funding. This change was intended to address two key concerns about solvency funding, namely, the significant additional funding requirements and the volatility inherent in solvency funding. This memo will analyze the practical impact of the implementation of the PfAD.

The PfAD is determined as a percentage that gets applied to a pension plan’s liabilities and current service cost. The impact on the balance sheet is that benefits cannot be improved until the liabilities plus PfAD is fully funded and remains fully funded after the improvement. Plans are not required to allocate contributions to fund the PfAD on the balance sheet.

The PfAD is considered an additional cost of benefits. Contributions must be sufficient to provide for the cost of benefits being earned, applicable expenses, the PfAD applied to the current service costs and any unfunded liabilities amortization amounts. The appendix provides a summary of the PfAD components across Canada applicable to target benefit multi-employer pension plans.

The following table provides the actual PfADs by year (as of December 31) for one actual Alberta registered Collectively Bargained Multi-Employer Pension Plan (given the PfAD formula, a similar outcome would occur for BC registered plans).

| Year | PfAD % |

| 2014 | 20.25% |

| 2015 | 19.50% |

| 2016 | 20.70% |

| 2017 | 26.10% |

| 2018 | 22.35% |

| 2019 | 32.40% |

It should be noted that during this period, there was no material change in the plan’s target asset mix. Despite this consistency, the year-end PfAD varied by 12.9 percentage points (19.5% to 32.4%). A more granular review of the PfAD, say quarterly or monthly, would illustrate even further volatility than what is illustrated by the year-end data points above.

One can make the following observations from the application of the PfAD funding requirement:

(a) There is a significant variability in the PfAD year by year.

(b) The absolute level of the PfAD is extremely high.

(c) There is excessive conservatism if contributions must be sufficient to fund the PfAD and amortize any unfunded liability.

This analysis does not address important aspects of the PfAD, such as what constitutes an “equity”1.

.

Although likely less onerous than solvency funding, the application of the PfAD does not eliminate the noted key deficiencies of solvency funding.

The variability of the PfAD means that the contribution sufficiency will be highly variable as well. This is counter to a basic tenet of such plans – benefit stability. Since contributions are fixed, funding variability can only result in benefit variability. This makes financial management very difficult and erodes member confidence in trustees, despite prudent, effective, efficient management by trustees. Member confidence further eroded in pension plans and in governments that approve rules that detract from pension plan sustainability. This outcome is solely due to PfAD structure.

Trustees are charged with the prudent management of the pension plan and owe plan beneficiaries a fiduciary duty. Thus, trustees should consider maintaining a margin/reserve/PfAD based on the circumstances of the plan. Trustees may consider a reserve of 20% - 25% appropriate for their plan, but when this is the legislated funding minimum, the impact of not achieving this level of funding is a reduction in benefits. This is simply unworkable. Minimum funding requirements with a large PfAD, like those in Alberta and BC, result in a rigid “one size fits all” approach that limits the trustees’ ability to manage the plan prudently for its specific circumstances. If minimum funding is to require a PfAD, the amount of, and formula for, the PfAD applicable to Limited Liability Plans in Saskatchewan would be more in line with what could be feasible for CBMEPPs.

The requirement to fund both the PfAD and any unfunded liability exacerbates the impact of variability and very high PfAD amounts. During periods of challenging experience, requiring funding of both the PfAD while amortizing an unfunded liability will, for many plans, result in benefit reductions. When the situation improves, the rules don’t permit such reductions to be restored (unless the PfAD is fully funded on the balance sheet). Even in the case of a fully funded plan with a healthy contribution margin, it can easily take in excess of 10 years to attain the level of funding required to be able to grant benefit improvements (or restore any benefit reductions). Requiring this level of funding, and as a result waiting period, to grant benefit improvements or restore past benefit reductions worsens the intergenerational inequities created by this PfAD framework. This excessive requirement is an impediment to the trustees’ fiduciary duty to act in the best interest of plan members. Therefore, benefit improvements and restoration of past benefit reductions should be allowed if the plan’s contributions are able to support the cost of the change, including the PfAD on the current service cost.

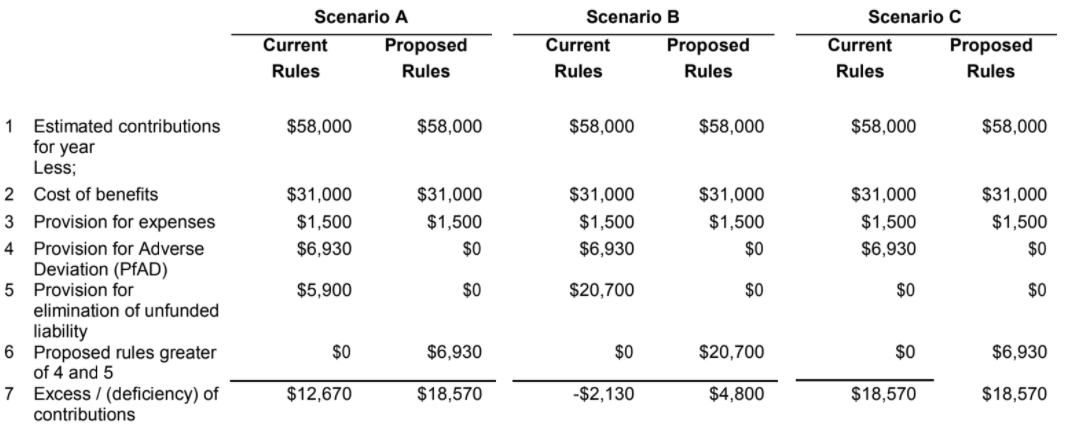

The requirement to fund both the PfAD and any unfunded liability also results in “double counting” that is counter to the purpose of the PfAD in the first place. If minimum funding is to require a PfAD, it should require that the PfAD on the current service cost should only be required if the plan is fully funded. A more appropriate application would be to require a provision of the greater of the PfAD and the amount required to eliminate any shortfall (the “Proposed Rules” in the illustrations below). This would ensure that any shortfall be eliminated and once achieved, the PfAD on the current service cost can recommence.

The following examples illustrate the double counting that results from the current requirements and the comparative requirements under the Proposed Rules, which eliminate this issue. The example includes the funding requirements for a plan with a 22.35% PfAD requirement under the following scenarios:

The above examples illustrate that:

Following the introduction of PfADs for Target Benefit Plans (TBPs) in BC in 2015, the BC Regulations were amended effective December 31, 2019 to introduce PfADs for non-Target Benefit Plans. The PfAD calculation for non-TBPs is simply 5 times the long bond rate (CANSIM Series V122544), subject to a minimum of 5% and further adjustment if the plan non-fixed income asset allocation is less than 30% (a proxy to recognize plans which have de-risked, typically on a path to wind-up). As of December 31, 2019, the long bond rate was 1.67%, generating a PfAD of 8.35% for plans subject to no further adjustments. This is significantly below the typical PfAD required for TBPs, even taking into consideration that non-TBPs are still subject to solvency funding, although the solvency ratio for funding has been reduced from 100% to 85%. Putting aside solvency funding, a PfAD of 32.40% as of December 31, 2019 for a TBP equates to the long bond rate being 6.48% to generate the same PfAD for a non-TBP. This represents a significant difference between TBPs and non-TBPs which is difficult to justify even after considering the impact of solvency funding for non-TBPs. It is not clear of the public policy reason imposing more onerous funding requirements for benefits that are not guaranteed vs. those plans with guaranteed benefits.

The Alberta and BC funding regimes impose unduly conservative regulated requirements which limit the trustees’ ability to manage the plan prudently for its specific circumstances. This will result in pension contributions of one generation be allocated to the PfAD and held indefinitely, reallocating these assets from one generation of member to another. Such actions can only jeopardize the long-term viability of such plans.

The funding requirements should support the public interest of protecting member benefits and foster the expansion of pension coverage. The result of these funding rules may in fact achieve the exact opposite. Addressing the above noted concerns and resolving these issues would go a long way to encourage confidence in these pension plans and expansion in pension coverage.

Yours truly,

Robert Blakely

President

robertblakely@mebco.org

1 The BC Regulations define an equity as “securities listed on a securities exchange, and includes any other investments that the superintendent has, in a record published by the superintendent, recognized as equities”, which is open to significant interpretation. In contrast, the Saskatchewan Regulations simply refer to the “the percentage of the assets of the limited liability plan that is invested in equities”.

The expert voice of multi-employer benefit interests in Canada.

Join Today!